JEFF JACOBY: A PONZI SCHEME….THAT’S NOT THE POINT

http://www.jeffjacoby.com/10235/a-ponzi-scheme-that-not-the-point

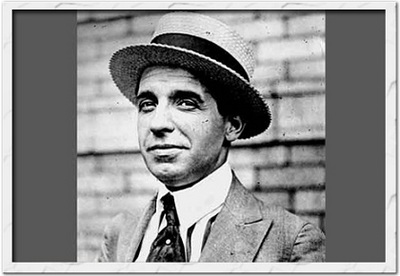

CHARLES PONZI was a Boston swindler who in 1920 bilked thousands of people out of millions of dollars by selling them bonds that guaranteed a fabulous rate of return — 100 percent in just 90 days. The funds entrusted to Ponzi were never invested in legitimate enterprises. Instead, they were deployed in a classic pyramid scam: The first few investors were paid off with money collected from a larger, second round of investors, whose bonds were in turn paid off with money from a still larger group of investors who came after them. Like all pyramid swindles, which depend on a steadily expanding population of new investors, Ponzi’s scheme was unsustainable. It collapsed within months. Ponzi went to prison, and his victims lost most of their principal.

Is Social Security just another Ponzi scheme? Texas Governor Rick Perry is only the latest public figure to make that claim. It’s an analogy that provokes heated debate — not surprising, given Social Security’s powerful emotional and philosophical resonance. That might not be a bad thing, if the debate moved Americans closer to solving the program’s long-term problems. But it doesn’t.

For years, notable voices — from the late economist Milton Friedman to Senator John McCain to former Slate editor Michael Kinsley — have warned that Ponzi’s ripoff was no different in principle from Social Security. Just as Ponzi’s scheme — or the more recent fraud by Bernard Madoff — eventually crumbled when there weren’t enough new investors to fund the payouts to the earlier investors, critics argue, Social Security will also fall apart as taxes paid into the system are outstripped by the benefits paid out.

That’s the point Perry was making last month, when he called it “a monstrous lie” that younger workers paying into Social Security today can rely on collecting benefits when they retire. “It is a Ponzi scheme for these young people,” he told an audience in Iowa. In interviews last fall, he made the same comparison.

But every analogy goes only so far, and there are flaws in this one too. Boston University journalism professor (and former Globe reporter) Mitchell Zukoff, who in 2005 published the definitive history of the Ponzi scandal, notes the dissimilarities. Ponzi’s scheme was a deliberate swindle that lured its victims with bald lies and get-rich-quick promises, Zuckoff has written, whereas Social Security fully discloses its operations and makes no promise of huge returns. Ponzi schemes are intended to defraud; Social Security was designed to be a social safety net for the old.

The Social Security Administration itself tackles the issue in a 2,400-word essay that not surprisingly concludes that there is no comparison between a pyramid scheme like Ponzi’s and the government’s 75-year-old pay-as-you-go pension program. The key difference: The former depends on a never-ending geometric increase in the number of participants, whereas Social Security is simply a financial “pipeline” that transfers income from current workers to current retirees. “As long as the amount of money coming in the front end of the pipe maintains a rough balance with the money paid out, the system can continue forever.”

Charles Ponzi bilked millions of dollars from thousands of duped investors through a pyramid swindle in 1920. Debating whether Social Security is another “Ponzi scheme” avoids the real issue. Charles Ponzi bilked millions of dollars from thousands of duped investors through a pyramid swindle in 1920. Debating whether Social Security is another “Ponzi scheme” avoids the real issue. |

Ah, but that’s the key question: Can that “rough balance” be maintained? When Social Security began, there were dozens of workers paying taxes into the system for every retiree who was taking benefits out of it. By 1950, the ratio had slipped to 16.5-to-1. Now it is a little less than 3-to-1, and continuing to shrink. When the last of the baby boomers retire, there will be just two working taxpayers for every beneficiary. In the face of such a demographic tide, isn’t Social Security ultimately as doomed as any pyramid scheme?

And yet whole furor over Social Security’s “Ponzi-ness” has mostly served as a giant distraction. Back and forth the arguments go — one side notes with alarm the exploding number of retirees, while the other side says Social Security taxes and benefits can always be adjusted. One side warns that Social Security’s future unfunded liabilities already amount to a staggering $20 trillion; the other side points to its huge current surpluses.

But fighting over an analogy gives both sides too easy an out. What Americans should really be wrestling with is not whether Social Security is or isn’t a Ponzi scheme, but whether its all-important surpluses are wisely invested. Or whether, to be precise, they are invested at all.

Next: Uncle Sam’s IOUs

(Jeff Jacoby is a columnist for The Boston Globe. His website is www.JeffJacoby.com).

— ## —

Comments are closed.